2025 was characterised by widespread double-digit returns, lifting many strategies to the top of performance tables and drawing understandable investor attention. In these environments, capital gravitates toward the leaders, and strong returns are often taken as evidence of superior skill. However, returns on their own are an incomplete measure. They do not capture how those outcomes were achieved, or how a portfolio is likely to behave when conditions change.

That distinction matters. Periods of strong performance often coincide with rising concentration, elevated valuations and a gradual build-up of risk beneath the surface. When that risk is eventually tested, outcomes can diverge quickly.

Recent experience within the South African long/short equity universe reflects this clearly. While many strategies have delivered broadly comparable long-term returns, the paths taken have differed meaningfully.

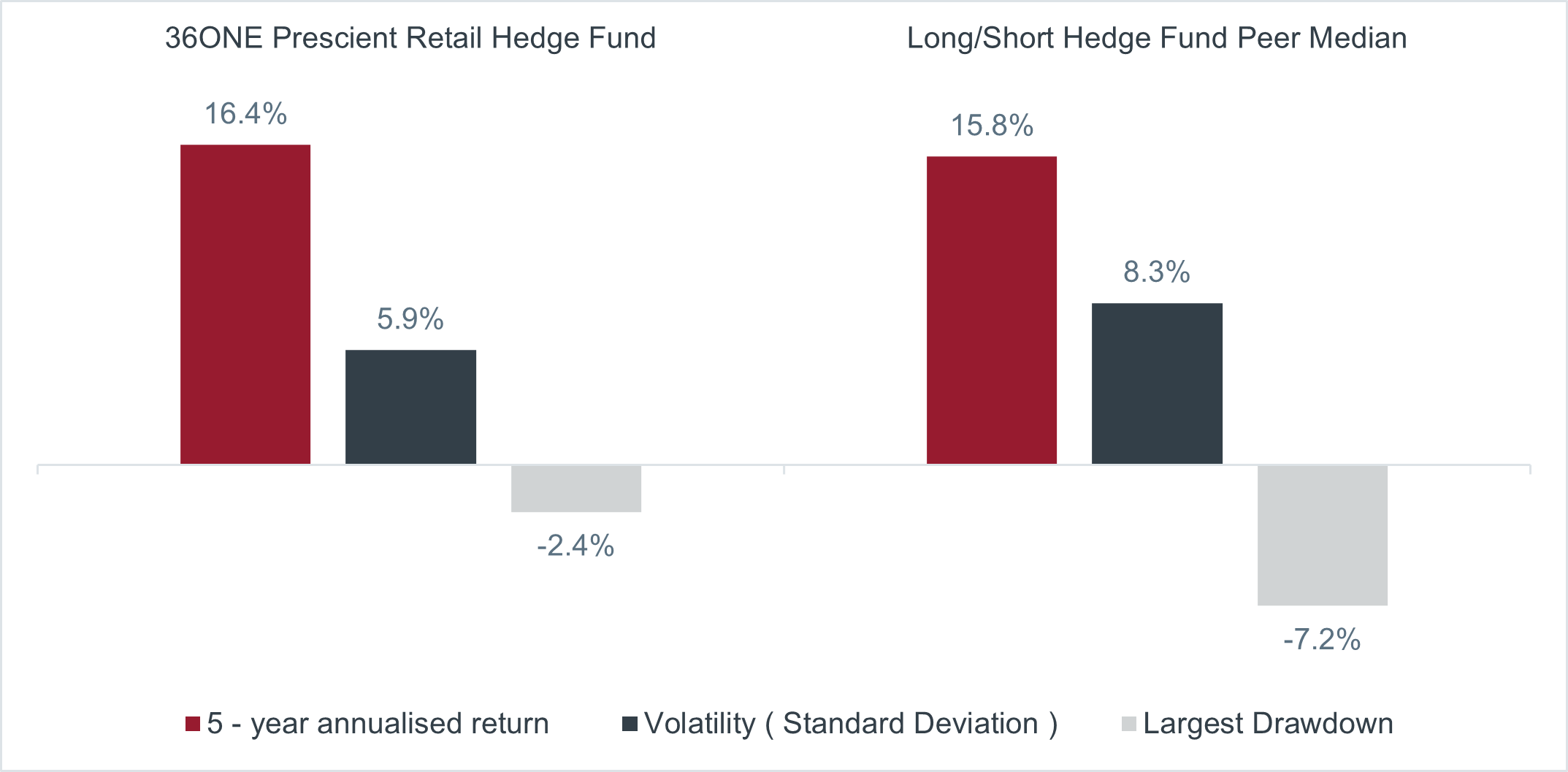

As illustrated below, the distinction is not in the return outcome alone, but in how that return was achieved. We compared the 36ONE Prescient Retail Hedge Fund to its peer group of 29 funds in the South African Long Short Equity category, that have a complete 60-month return history ending 31 December 2025. The 36ONE Prescient Retail Hedge Fund has delivered a five-year annualised return of approximately 16.4%, broadly in line with its peer group. However, this has been achieved with materially lower volatility (5.9% vs 8.3%) and a significantly shallower maximum drawdown (-2.4% vs -7.2%). This difference is not incidental. It reflects a more controlled risk profile, where capital preservation during periods of stress is prioritised alongside return generation. A deeper drawdown changes the starting point for recovery and increases the burden on future returns. Over time, these differences compound, shaping both the consistency of outcomes and the overall investment experience.

When it mattered

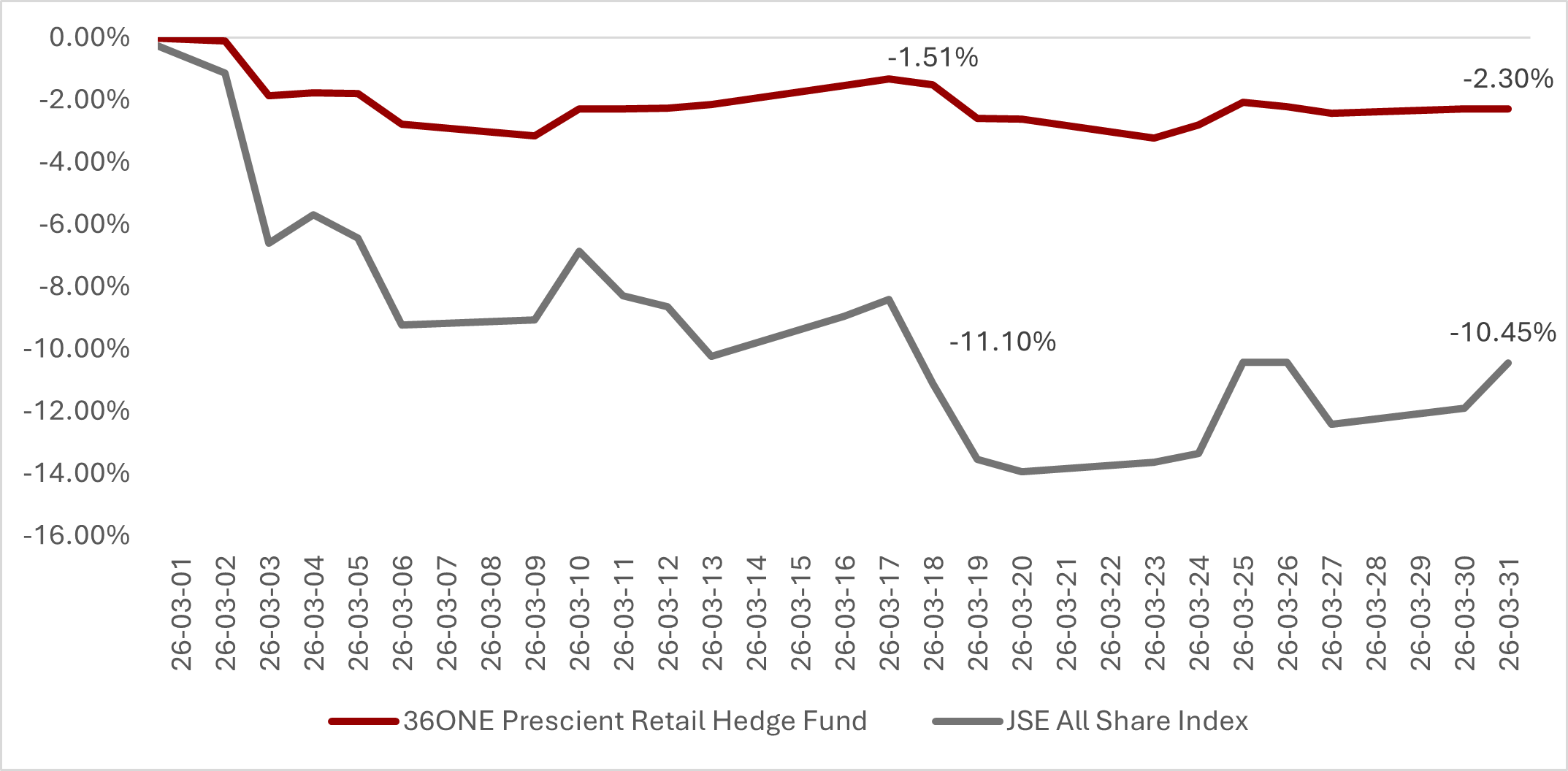

This became particularly evident during the escalation of the US - Iran conflict in March 2026. As geopolitical tensions intensified, markets reacted sharply, with the FTSE/JSE All Share Index declining by more than 13% month-to-date at its weakest point.

The initial phase of the sell-off, as the conflict first entered the news cycle in early March, was especially telling. Within the long/short equity hedge fund universe, dispersion in outcomes was pronounced. Several funds experienced drawdowns of between 8% and 16% over a relatively short period, reflecting differing levels of net exposure and sensitivity to the broader market. Against this backdrop, the 36ONE Prescient Retail Hedge Fund declined approximately 1.5% month-to-date as at 18 March 2026, remaining within a relatively narrow range despite the severity of the sell-off. (Source: MoneyMate, 01–18 March 2026).

This was not a function of timing or a single position. It reflects how the portfolio is constructed. Net exposure is actively managed, and downside protection is implemented ahead of periods of stress, not in response to them. The objective is not to avoid volatility altogether, but to limit participation in broad-based drawdowns when they occur. The result is a different return profile. When markets fall sharply, the aim is to lose less. Over time, that distinction becomes meaningful. Drawdowns alter the starting point for recovery, and reducing their magnitude lowers the hurdle required to rebuild capital.

This is evident in the return path shown in the graph below. As the market moved sharply lower, the fund’s returns declined more gradually and stabilised earlier, while the broader index continued to fall and remained materially weaker throughout the period. The divergence widened as the sell-off progressed, illustrating how limiting downside participation can meaningfully alter cumulative outcomes over even short timeframes.

Market conditions today make this approach increasingly relevant. Equity returns, both globally and locally, remain concentrated in a relatively small number of companies. At the same time, geopolitical risk has become a persistent feature of the investment landscape rather than an occasional disruption. In this environment, strong headline returns can coexist with elevated underlying fragility. The ability to adjust exposure, introduce hedges, and allocate capital selectively becomes less of an advantage and more of a necessity.

At 36ONE, this is not a theoretical framework but a core part of how portfolios are managed. The purpose of a hedge fund is not simply to participate in rising markets, but to actively manage risk and protect capital during periods of stress. Ultimately, the objective is to deliver consistent, risk-adjusted returns by limiting downside participation when markets fall. The difference between simply participating and actively protecting capital is often only visible when it matters most.